bike insurance should be straightforward — but for many two-wheeler owners, the sheer number of options, policy types, and technical terms makes it confusing. Comprehensive or third-party? High IDV or low? Which add-ons are actually worth paying for?

This guide cuts through the noise with practical tips to help you select the right bike insurance without second-guessing yourself.

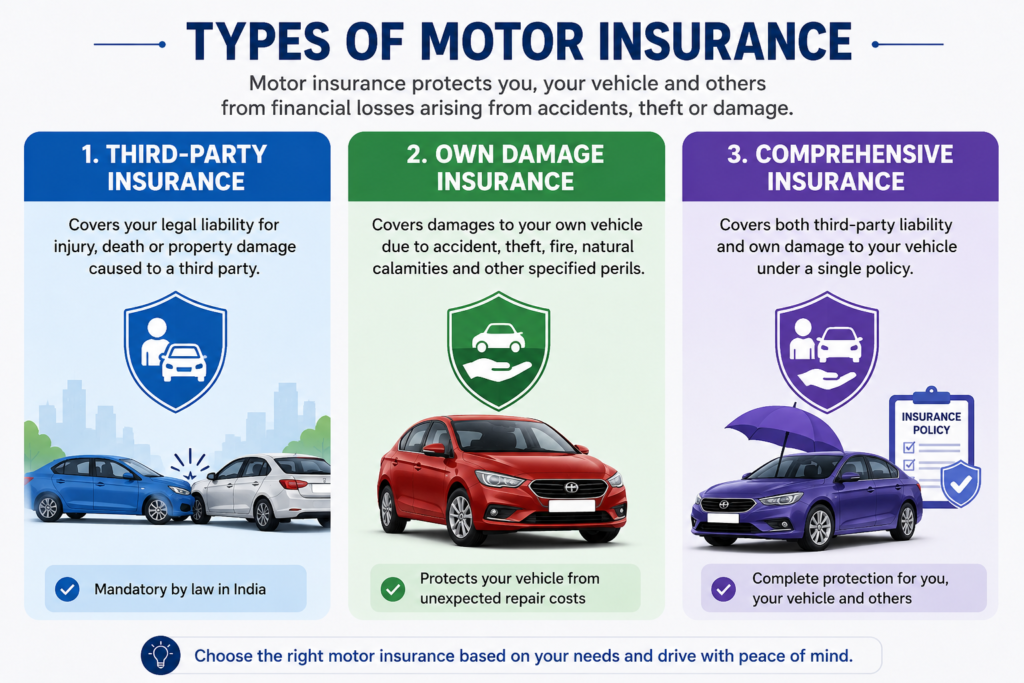

Understand the Types First

Before comparing specific policies, get clear on the types of motor insurance available for two-wheelers:

Third-Party Only: Covers liability for injury or damage caused to others. Legally mandatory. Does not cover your own bike.

Comprehensive: Covers third-party liability plus damage to your own bike from accidents, theft, fire, flood, and natural calamities. Significantly broader protection.

Standalone Own-Damage: Covers only your own bike’s damage. Purchased alongside a separate third-party policy. Useful if you want to switch own-damage insurers without affecting your long-term third-party cover.

For most active riders, a comprehensive policy offers the best value. Third-party-only cover makes sense for very old bikes where the repair cost exceeds the bike’s current market value.

Tip 1: Set the Right IDV

The Insured Declared Value (IDV) is the maximum amount your insurer will pay if your bike is stolen or declared a total loss. It directly reflects your bike’s current market value.

- Too low an IDV reduces your premium but leaves you under-compensated in a total loss scenario.

- Too high an IDV unnecessarily inflates your premium.

Use an IDV calculator to arrive at the correct figure before you buy. The right IDV should closely match the realistic resale price of your bike in the current market.

Tip 2: Prioritise Claim Settlement Ratio Over Premium

The single most important number when evaluating an insurer is its Claim Settlement Ratio (CSR) — the percentage of claims settled out of total claims received. IRDAI publishes this annually.

Choose insurers with CSRs above 95%. A slightly higher premium from a high-CSR insurer is almost always better value than a cheaper policy from one that rejects a significant proportion of claims.

Tip 3: Choose Add-Ons Thoughtfully

Add-ons extend your coverage beyond the base policy. For bikes, the most valuable ones include:

Zero Depreciation Cover: Without this, depreciation is deducted from the payout for replaced parts. With it, you receive the full replacement cost. Essential for bikes under 5 years old.

Roadside Assistance: Covers towing, minor on-site repairs, and emergency fuel delivery. Very useful for long commuters and those riding in areas away from service centres.

Engine and Gearbox Protection: Covers damage to engine and transmission — typically excluded from standard comprehensive policies unless caused by a direct accident.

Return to Invoice: In case of theft or total loss, pays you the original invoice price of the bike rather than the depreciated IDV. Ideal for new bikes.

Personal Accident Cover for Pillion: The standard policy only covers the owner-rider. If you regularly carry a pillion, adding cover for them is prudent.

Don’t buy every available add-on indiscriminately — assess which ones match your actual riding patterns and risk exposure.

Tip 4: Check the Cashless Garage Network

Cashless repairs mean your insurer settles the repair bill directly with the authorised garage — you pay only the deductible. For this to be useful, your insurer must have empanelled garages for your bike’s brand in your area.

Before purchasing, check the cashless garage network for your city. If you ride a premium or less common brand, network coverage matters more.

Tip 5: Don’t Let Your NCB Go to Waste

Your No Claim Bonus (NCB) is a discount earned for each claim-free year. It accumulates up to 50% on the own-damage premium over five years. If you switch insurers, request an NCB retention certificate from your existing insurer — the NCB transfers with you.

For small claims that barely exceed your deductible, calculate whether claiming is worth losing your NCB. Often, paying out of pocket for minor repairs is the smarter choice.

Tip 6: Buy or Renew Online

Online purchase of [bike insurance](www.bajajfinserv.in/insurance/two-wheeler-insurance-all-products) is faster, paperless, and often cheaper — insurers save on agent commission and pass some of that saving to online buyers. Compare quotes from multiple insurers on a single platform, check IDV, add-ons, and exclusions side by side, and purchase in minutes.

Tip 7: Read the Exclusions Carefully

Every policy has a list of circumstances under which claims are not payable. Common exclusions include:

- Riding without a valid licence

- Riding under the influence of alcohol or drugs

- Damage caused outside India

- Consequential damage (e.g., engine damage from riding through a flooded road, unless you have engine protection add-on)

- Normal wear and tear

Understanding exclusions before you buy prevents unpleasant surprises when you file a claim.

Tip 8: Renew Before It Lapses

A lapsed policy means riding illegally. It also means losing your accumulated NCB if the lapse exceeds 90 days. Set a calendar reminder at least 30 days before your policy expiry date — renewing on time costs nothing extra and preserves all the benefits you’ve built up.

Making the Final Decision

There is no universally “best” bike insurance policy — the right one depends on your bike’s age and value, how frequently you ride, your city’s traffic conditions, and your financial ability to absorb unexpected repair costs.

Use a comparison platform to evaluate at least three policies simultaneously. Focus on CSR, IDV accuracy, cashless garage network, and the add-ons that match your riding profile. Price matters — but only after these fundamentals are satisfied.

The right bike insurance isn’t the cheapest one — it’s the one that actually performs when you need it.